2 Information necessary to track progress made in implementing and achieving NDCs

2.1 National circumstances and institutional profile

2.1.1 National circumstances

Below, information is reported on national circumstances relevant to progress made in implementing and achieving Norway’s NDC under Article 4 of the Paris Agreement and how national circumstances affect GHG emissions and removals over time.

Government structure

Norway is a constitutional monarchy with a democratic parliamentary system of governance. The current Government (the Støre Government) took power in October 2021. It is a minority coalition between the Labour Party and the Centre Party. The Storting (Norwegian parliament) determines Norway’s overall climate policy, and the government implements and administers the policies and measures.

Although it is not a member of the EU, Norway has, since 1994, been part of the European Union’s internal market through the Agreement on the European Economic Area (EEA Agreement). The objective of the EEA Agreement is to strengthen trade and economic relations between the EEA/EFTA States and the EU Member States, based on a level playing field throughout the EEA. The Agreement gives the EFTA countries opportunities to influence EU policy making also in areas of relevance to the internal market, including environmental policies. A practical implication of the EEA agreement is that Norway adopts the same legislation as EU where relevant. Details on legislation relevant to climate change are given in chapter 2.5.

Population profile

With a total area of almost 324,000 km2 and only 5.5 million inhabitants, Norway has the lowest population density in Europe after Iceland and Russia. The large majority of the Norwegian population is settled along the coast and the fjords, and an increasing percentage, at present about 80 per cent of the population, lives in urban settlements. Most of the urban settlements are small and have under 20,000 inhabitants. Only six areas – Oslo, Bergen, Stavanger/Sandnes, Trondheim, Fredrikstad/Sarpsborg and Drammen – have more than 100,000 residents. More than a third of Norway’s population lives in the six largest city areas. Population has grown from 4.2 million in 1990 to 5.5 million in 2023, about 31 per cent.

Geographical profile

The mainland of Norway is 1,752 km from north to south, spanning about 13 degrees of latitude. The total area of the mainland is 323,781 km2. In addition, the Norwegian continental shelf is 2,039,951 km2. The mainland coastline is more than 2,500 km long, excluding fjords and bays. In the east, Norway shares borders with Sweden, Finland and Russia. In addition, the Arctic archipelago of Svalbard is under Norwegian jurisdiction. Except for the LULUCF sector, the inventory includes emissions on the archipelago Svalbard as well as on mainland Norway. In particular, emissions from coal mining on Svalbard are included.

The long and narrow shape of Norway is accompanied by wide variations in climate, geology and topography. This gives large variation in conditions for land use. Only about 30 per cent of the land area is lowland below 300 meters, and this is where most people live and where agricultural production is most prominent. As much as 20 per cent of the land area is mountainous areas more than 900 meters above sea level. Cultivated land account for only 3 per cent of the mainland, while about 37 per cent is covered by forest. The remaining area consists of other cultivated and developed land, scrub, and heath along the coast, mountain forest and marginal forest, and sparsely vegetated mountains and mountain plateaus. About 46 per cent of the land is above the tree line. Currently, 25.7 per cent of the land area including Svalbard and Jan Mayen is protected under the Nature Conservation Act and the Svalbard Environmental Act. Of the Norwegian mainland, 17.6 per cent is protected. Nevertheless, the proportion of wilderness-like areas, defined as areas more than 5 km from major infrastructure development, has been reduced dramatically from about 48 per cent of the land area in 1900 to about 11.2 per cent today. From 1988 to 2023 this area was reduced with about 2890 km2. Only about 5 per cent of the area of southern Norway is characterised as wilderness-like.

Economical profile

Norway is a small, open economy. In 2023, exports constituted about 47 per cent of GDP. Together with foreign shipping, the production of crude oil and natural gas account for about a fourth of GDP in Norway, but only a small proportion of employment, see Table 2.1. Around 30 per cent of the workforce are employed in the public sector.

Tabell 2.1 GDP and employment in 2023

GDP (2023 prices, million NOK)

Share of Total GDP

Employment (1000 persons)

Share of total employment

Norway

4,643.1

1.00

2,968.1

1.00

Mainland Norway

3,420.2

0.74

2,923.6

0.98

Public sector

841.5

0.18

889.5

0.301

Oil and gas extraction2 and foreign shipping

1,222.9

0.26

44.5

0.02

1Share of the employment in mainland Norway

2Including transport via pipelines

Source: Statistics Norway

Norway has greatly benefitted from cross-border trade and investments. Globalisation facilitates access to financing, capital and labour inputs, export markets, technological transfers, and increases competition. The result is a more efficient use of available resources, which has contributed to strong global growth during the past decades. Norway has for a long time benefitted from rising export prices and falling import prices. However, the Norwegian krone has weakened in recent years. This depreciation has increased profitability in export-oriented industries, but at the same time it contributes to higher import prices and costs for households and businesses that purchase goods and services from abroad.

High price growth, combined with higher interest rates to combat inflation, has reduced the growth in activity in the Norwegian economy. Growth is now lower than the initial period following the global Covid-19 pandemic. The labour market is however still characterized by high demand for labour and the unemployment is low.

The petroleum industry remains important for the Norwegian economy for years to come, but as share of GDP it is expected to decline as remaining resources are depleted.

A continually stricter global climate policy and an ever faster technological development changes the overall conditions for Norwegian business. Norway’s ambitious climate goals require higher growth and new jobs in less carbon-intensive sectors. The strategy for green competitiveness sets the direction for this change.

The emissions for 2023 were published by Statistics Norway in November 2024. The numbers for 2023, that have not yet been reported to the UNFCCC, show that Norway’s emissions totalled 46.7 million tonnes of CO2 equivalents, excluding LULUCF. This is a decrease of 9.1 per cent since 1990, and a 4.7 per cent decrease from 2022 levels.

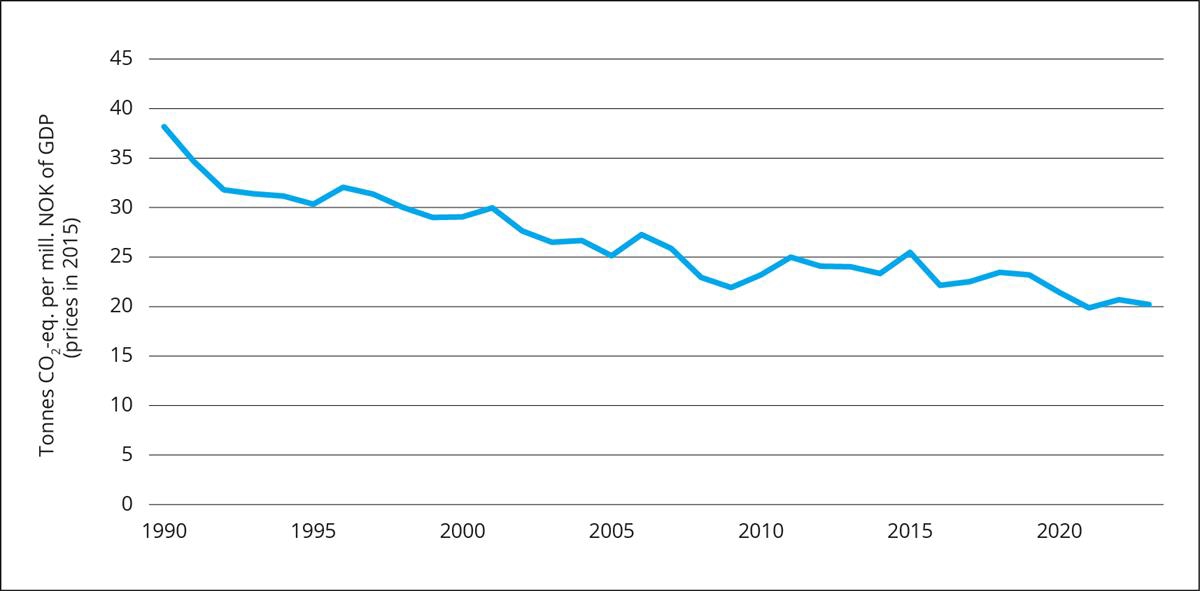

Emission intensity fell by 56 per cent from 1990 to 2022 (see Figure 2.1). Emission intensity does not include inflation. Greenhouse gas emissions relative to GDP normally decline as scarce resources are utilised more efficiently. Use of taxes or quotas on emissions, resulting in higher energy costs, reinforce this trend. Norway introduced a CO2 tax as early as 1991. This tax has subsequently been supplemented by the participation of Norwegian installations in the EU’s emissions trading system. About 85 per cent of all greenhouse gas emissions in Norway are subject to economic instruments. The use of economic instruments has contributed to the significant decline in emission intensity.

Figur 2.1 Emission intensity in Norway

Source: Statistics Norway

Climate profile

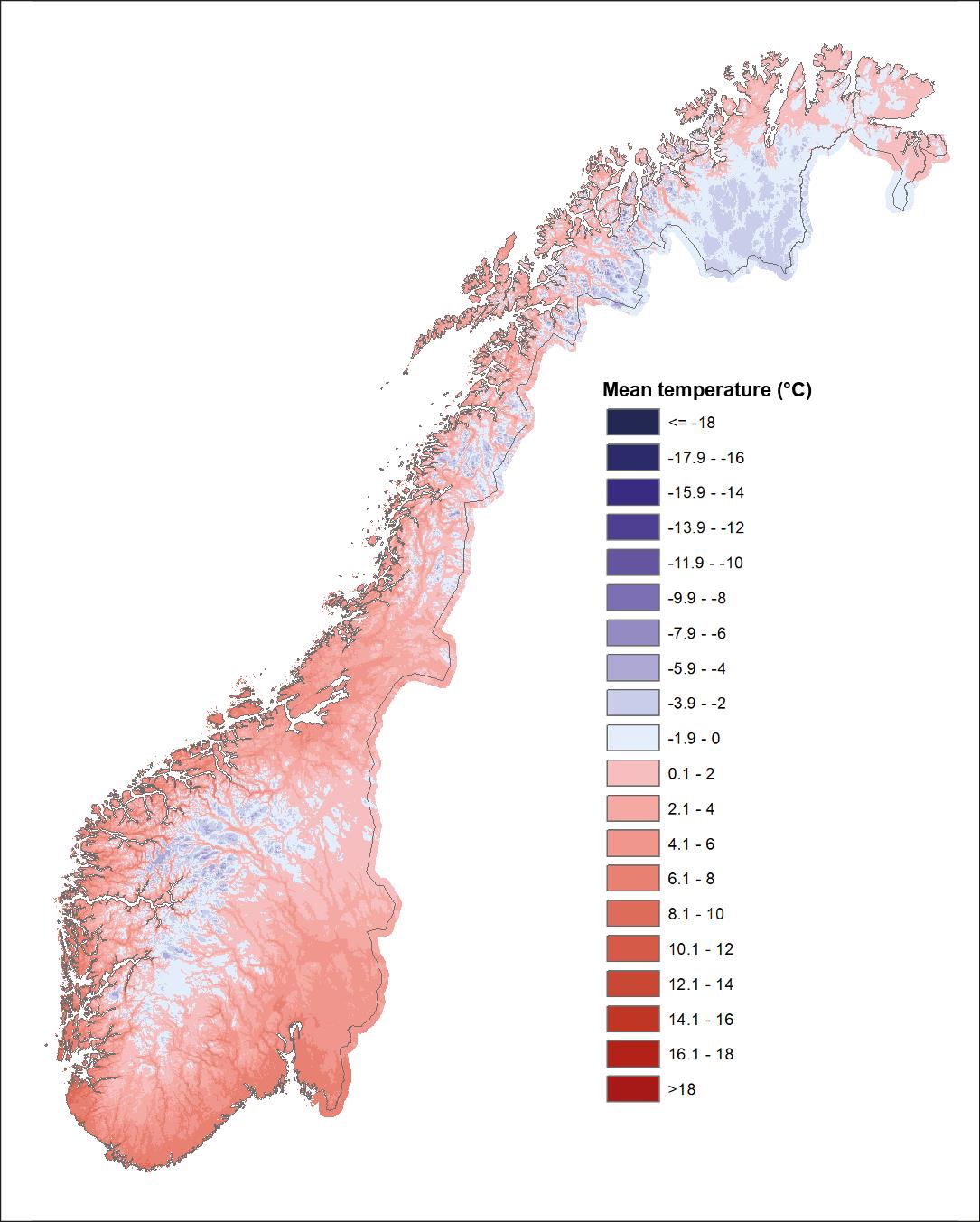

Because of the influence of the North Atlantic Ocean, Norway has a much warmer climate than its latitudinal position would indicate. Therefore, most of Norway has a maritime climate with relatively mild winters and cool summers. On an annual basis, the highest normal (1991–2020) annual air temperatures, (up to 8.6°C) are found along the south-western coast (see Figure 2.2). Outside the mountain regions, the lowest annual mean temperatures (down to -1.9°C) are found on the Finnmark Plateau. During winter, the coast from Lindesnes to Lofoten has normal monthly mean temperatures above 0°C. The absolute lowest and highest temperatures measured at official weather stations on the mainland are -51.4°C and +35.6°C, respectively.

In the cool Norwegian climate, there is a substantial need for heating of buildings. The «heating degree days» (defined as the number of degrees the daily mean temperature is below 17 °C, added up for every day of the year) for the 1991-2020 period was between 3,000–4,000 in the coastal lowland areas. In the northernmost parts of Norway, the value can be up to 7,000.

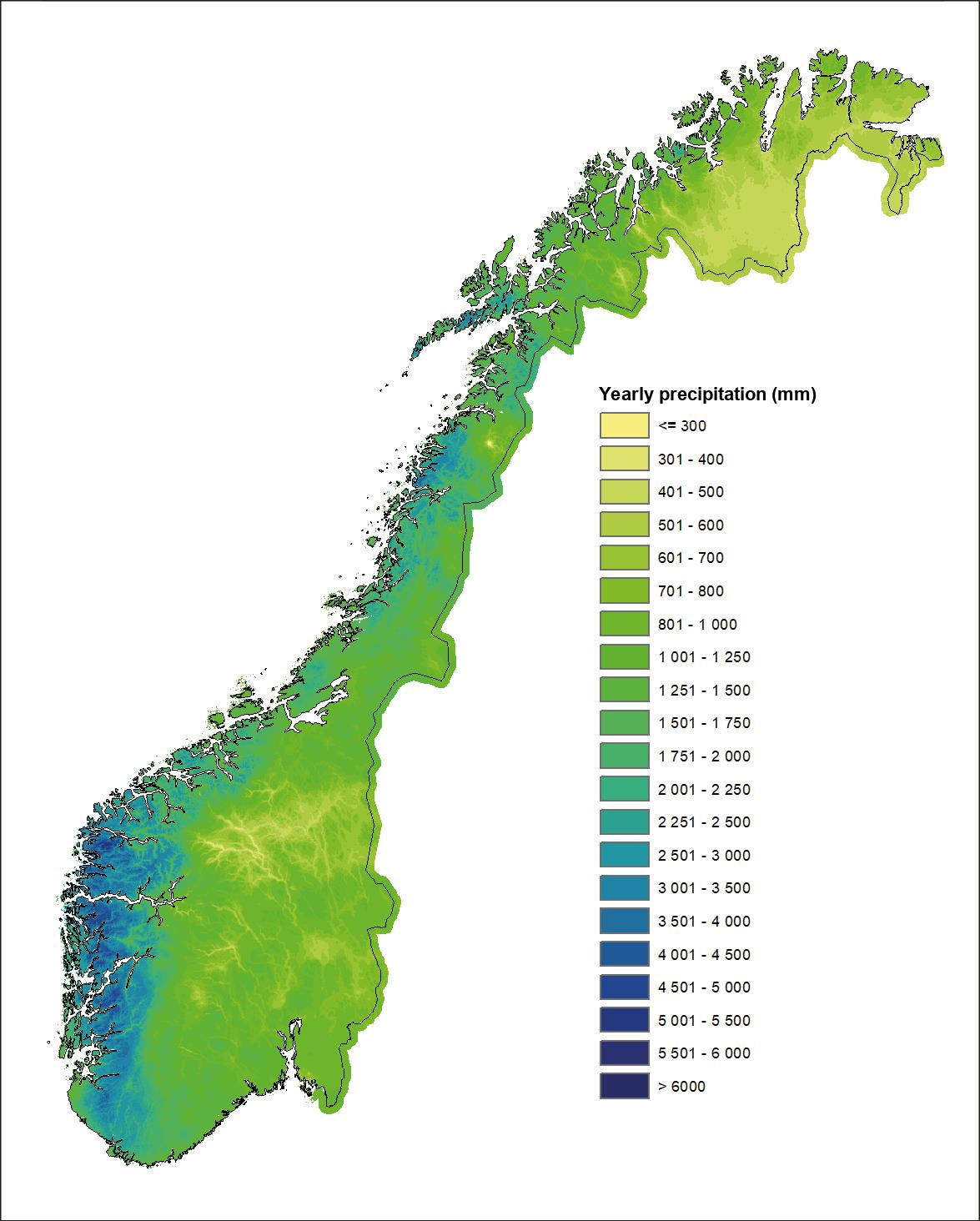

Because of prevailing westerly winds, moist air masses flow regularly in from the ocean giving abundant precipitation over most of Norway. Areas just inland of the coast of western Norway get the most precipitation (see Figure 2.3). This zone of maximum precipitation is one of the wettest in Europe, and several sites in this region have normal annual precipitation of more than 3,500 mm. On the leeward side of the mountain ranges, the annual precipitation is much lower, and a few sheltered stations in the inland areas of south-eastern Norway and one station in Nordland have normal annual precipitation less than 350 mm.

Figur 2.2 Normal annual temperature in Norway 1991–2020

Source: Norwegian Meteorological Institute

Figur 2.3 Normal annual precipitation in Norway 1991–2020

Source: Norwegian Meteorological Institute

2.1.2 Sector details

Energy

Energy use and electricity production

Nearly all of Norway’s electricity production is based on renewable energy sources, and the proportion of energy use accounted for by electricity is considerably higher than in most other countries.

Norway has a large energy-intensive manufacturing sector, and electricity is more widely used to heat buildings and water than in most other countries. Because renewable energy is the main source of energy usage, greenhouse gas emissions associated with stationary energy use are low in Mainland-Norway.7

Emissions to air from energy use are therefore mainly concentrated in manufacturing, transportation, construction, and agriculture where the use of fossil fuels is still widespread. Emissions to air from offshore petroleum activities largely originate from the combustion of natural gas and diesel in turbines, engines and boilers, flaring of natural gas for safety reasons, venting and diffuse emissions of gas, and storage and loading of crude oil.

Important drivers of energy use

There are various factors that influence the energy usage in Norway. Variations in energy use from year to year are often related to fluctuations in weather conditions and in the prices of energy and energy-intensive goods and services. Longer-term trends are related to population growth and other demographic factors, industrial structure and to the rate of economic growth and structural changes in the economy.

Norway’s population has grown about 31 per cent from 1990 to 2023. Strong economic growth has resulted in a tripled GDP since 1990. Both demand for goods and services that use energy are growing steadily. However, final energy consumption has risen by only 14 per cent, demonstrating that the Norwegian economy gradually has become less energy-intensive.

Norway has a national target to improve energy intensity in the mainland economy by 30 per cent from 2015 until 2030. The Ministry of Energy reports every year on the development in energy intensity in the state budget. In 2023 the government presented an action plan for energy efficiency, presenting several instruments that will contribute to more energy efficiency, including legal requirements and targeted information measures.

Energy usage, by sector

Energy use in absolute numbers is highest in the manufacturing and transport sectors, followed by households and services. Other sectors such as construction, agriculture, and fisheries account for only a small proportion of energy use. Energy use has increased since 1990, with most of the increase taking place before 2000. In 2023, the final energy consumption was about 217 TWh (Statistics Norway).

Electricity is the dominant energy carrier, followed by petroleum products. Electricity dominates energy use in manufacturing, the household sector and service industries, while petroleum products account for a large proportion of energy use in sectors that make heavy use of transportation and machinery. District heating account for only a small share of energy use, but this has been increasing in recent years. Consumption of district heating has risen slightly in recent years. These energy carriers have been replacing fossil fuels and petroleum products for heating and in industrial processes.

The energy intensity of the Norwegian economy has declined by 45 per cent since 1990. This indicates a decoupling of economic growth and energy use.

Per capita energy use has also declined in Norway during this period and was about 10 per cent lower in 2023 than in 1990.

Features of the Norwegian energy system

Renewable energy sources account for 98 per cent of Norwegian electricity production and the power sector has very low emissions compared to most other countries. In a normal year renewable electricity generation exceeds gross domestic consumption.

At the end of 2023, the installed capacity of the Norwegian power supply system was 40 077 MW with an estimated annual production of 157.8 TWh in a normal year.

Over the past few years, Norway has been developing more renewable power production capacity than it has done for over 25 years due to increased profitability for more renewable technologies. Wind power currently accounts for only a relatively modest share of production capacity, but between 2016 and 2022 the installed capacity increased from about 874 MW to about 5,073 MW. At the end of 2023, estimated annual wind power production corresponded to almost 17 TWh in a normal year. In recent years, the installed capacity of solar power has increased sharply, and in 2023 the installed capacity was doubled from about 300 MW to about 600 MW by the end of the year.

Hydropower accounts for approximately 88 per cent of Norwegian power supply, and the resource base for production depends on the precipitation levels between years. Norway has half of Europe’s reservoir storage capacity, and more than 75 per cent of Norwegian production capacity is flexible. Production can be rapidly increased and decreased and serves as an important provider of flexibility in the power system. This is a distinctive feature of the Norwegian power system.

The Norwegian power system is closely integrated with the other Nordic systems, both in physical terms and through market integration. In turn, the Nordic market is integrated with the rest of Europe through cross-border interconnectors with the Netherlands, Germany, the Baltic states and Poland.

In 2023, district heating deliveries totalled 7.9 TWh, about five times as much as in 2000. This is equivalent to about one sixth of the total energy consumption in households per year in Norway.

District heating can be produced using many different types of fuel. In 2023, almost 42 per cent of district heating was produced from waste and about 38 per cent from bioenergy. The use of petroleum products has declined since 2018. Mineral oil accounts for only 1 per cent of district heating production.

Bioenergy is an important energy source for heat production in Norway. Annual consumption of bioenergy in Norway rose from 10 TWh in 1990 to about 17.5 TWh in 2010. Since then, the consumption has varied and was about 20 TWh in 2023. Fuelwood consumption in households accounts for a large proportion of biofuel consumption and totalled more than 6 TWh in 2023. The second largest user is the manufacturing sector, where chippings and other wood waste are used as fuel in production processes.

The Norwegian government has an ambition to award areas that has potential for 30 GW of offshore wind capacity by 2040. In 2020, the first areas on the Norwegian continental shelf were opened for offshore renewable energy production. In 2023, Sørlige Nordsjø II was announced as the first project area, and, following a successful auction, was awarded in April 2024.

The Hywind Tampen wind farm is the world’s largest floating offshore wind farm, which supplies 88 MW of power to the Snorre and Gullfaks petroleum fields. In 2022, the Hywind Tampen was set in operation.

Petroleum

Petroleum activities have given substantial impetus to Norway’s economic growth and has helped finance the Norwegian welfare system. According to the Norwegian Offshore Directorates latest resource account, about half of the estimated recoverable resources on the Norwegian shelf have been produced and sold so far.

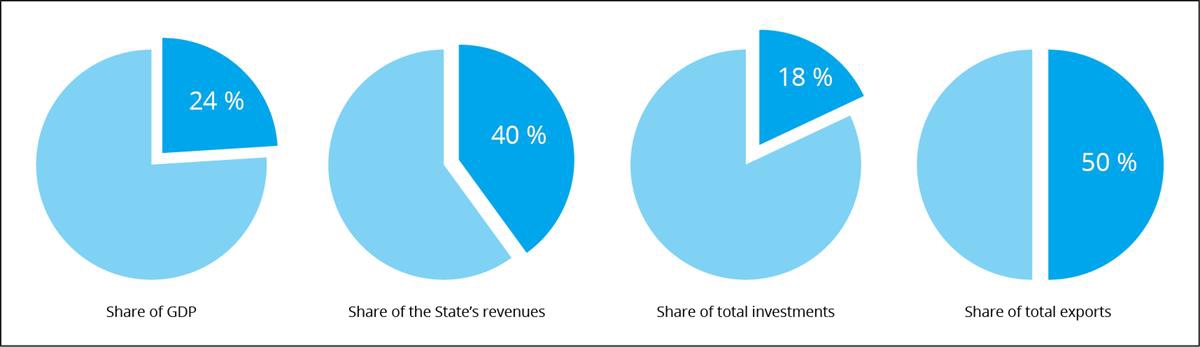

According to data for 2023 published by Statistics Norway in November 2024, greenhouse gas emissions from petroleum activities amounted to 11.6 million tonnes of CO2 equivalents in 2023. These emissions account for about a quarter of the total Norwegian greenhouse gas emissions. Emissions have increased by 40.1 per cent since 1990. Emissions peaked in 2015 and have declined since, mainly due to increased use of renewable power from shore on petroleum installations.

Figur 2.4 Macroeconomic indicators for the petroleum sector in 2023

The service and supply industry is not included.

Source: National Accounts, the National Budget 2025

Since production started, oil and gas have been produced from a total of 123 fields8 on the Norwegian shelf. At the end of 2023, 92 fields were in production: 67 in the North Sea, 23 in the Norwegian Sea and two in the Barents Sea.

In 2023, Norwegian petroleum production accumulated to 233.2 million Sm³ o.e., which is about the same level as production in 2022. By comparison, total production in the record year of 2004 was 264.2 million Sm3 o.e. Total production is expected to reach a peak in 2025, and then decrease over time.

Oil production in 2023 was higher than in 2022. The main reason is startup of production from new fields. Gas sales totalled 116 billion Sm³ (40 MJ) in 2023, a decrease from the production in 2022. The reason for the reduction is mainly extended maintenance activities on the onshore facilities. In 2023, natural gas accounted for 50 per cent of the total production measured in oil equivalents.

Like oil, gas is one of Norway’s most important export commodities. Domestic consumption of gas is low, and nearly all the gas produced is exported. An extensive network of subsea pipelines links Norway’s offshore gas fields and onshore terminals directly to recipient countries in Europe. In addition, liquefied natural gas (LNG) is shipped out from the Snøhvit field off Hammerfest on LNG carriers.

About 46 per cent of Norway’s estimated gas resources have been produced and sold so far. Gas production is expected to remain at a high level for the next years.

Norway is the largest producer and only net-exporter of oil and gas in Europe. In 2023, Norway exported about 116 billion Sm3 gas. In large parts of Europe, gas is an important source of energy for heating, industrial use and for electricity generation in gas-fired power plants. Norwegian gas now covers nearly 30 per cent of the EU’s and the UK’s combined gas consumption and provides an important contribution to energy security in Europe. The total length of the Norwegian gas pipeline network is about 8,800 kilometres. Most Norwegian gas sold in the European market is delivered to Germany, the UK, Belgium and France. In the short and medium term, Norwegian natural gas may support the phasing-out of coal in the European power sector, and may be an important co-player with renewables in the efforts to reduce emissions. Gas can be stored and serve as a flexible energy source for heat and electricity production, balancing supply and demand.

Transport

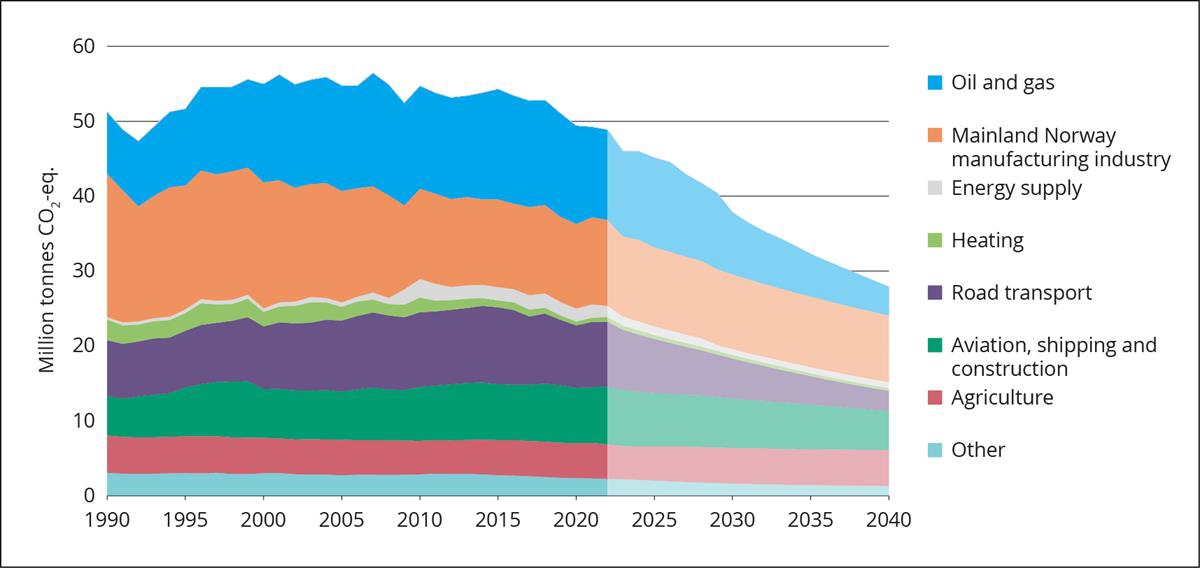

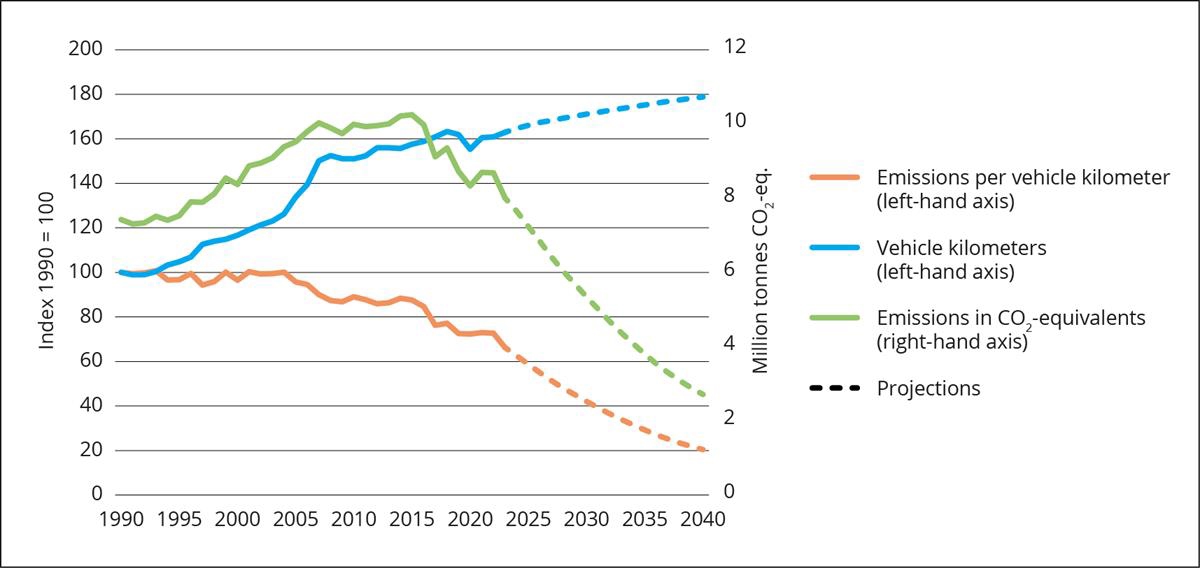

Norway’s decentralised settlement gives rise to a relatively high demand for transport. In addition, the Norwegian economy is largely based on the extraction of raw materials and exports of goods, which means that there is a large volume of goods transport. About one third of the total Norwegian greenhouse gas emissions originated from transport in 2023.

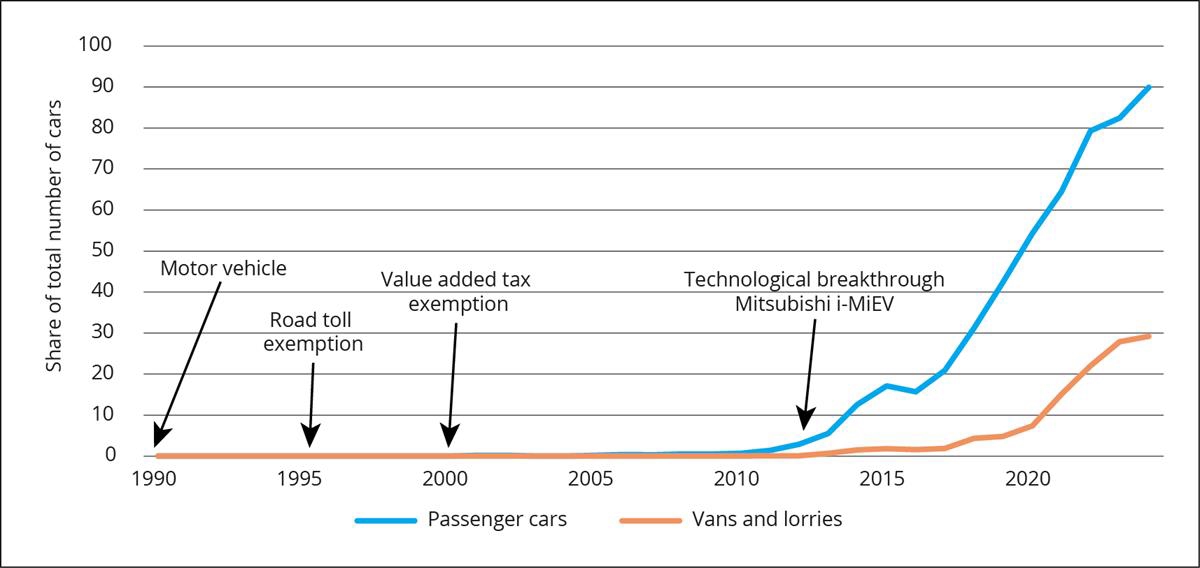

According to data for 2023 published by Statistics Norway in November 2024, the emissions from road transport were approximately 8 per cent above 1990-levels in 2023. Road transport emissions have decreased since 2015, partly due to biofuels replacing fossil fuels. The rise in zero-emission vehicle usage is another factor contributing to the reduction in road transport emissions. The market share for electric vehicles has increased steadily in recent years. So far in 2024, electric vehicles has had a market share close to 90 per cent for new passenger cars, while in 2020 the share was 53 per cent. For light-duty vehicles, the market share for new electric vehicles has risen from 9 per cent in 2020 to almost 30 per cent so far in 2024. Also, for heavy duty vehicles there has been an increase in the market share of electric vehicles in the recent years. Electric city buses had a market share of almost 70 per cent so far in 2024. For long distance buses and trucks, the development has been somewhat slower. So far in 2024, electric long-distance buses and trucks held market shares of 24 per cent and 12 per cent, respectively. These shares are expected to increase in the coming years, driven by technological improvements and climate policies.

Since more than 80 per cent of railway traffic in Norway is electric, railway transport only account for a small share of the total emissions. Direct emissions from the railway sector mainly comes from transport on the diesel driven tracks, and from construction, operations and maintenance of the railway infrastructure. Emissions from railways (including passenger and freight transport) has remained more or less constant at 50,000 tonnes CO2-equivalents in the last few years, accounting for about 0.1–0.3 per cent of the total emissions from the transport sector.

In 2023 there were 78.2 million railway passengers. Passenger traffic by railways was strongly affected by the pandemic. Even though there has been growth in recent years, there are still 2 million fewer passengers than in the peak year of 2019.

For domestic goods transport, there was an increase in tonne-kilometres from 2019 to 2023. For goods transport excluding cabotage, the increase was 11.1 per cent, while for goods transport including cabotage, the increase was 9.3 per cent. Transportation of goods by railways witnessed an increase during the pandemic but has decreased since 2021. In 2023 freight transport decreased with 7.5 per cent. The extreme weather event «Hans» and other weather events have led to increased and prolonged downtime on the railway network. In August 2023, the Randklev bridge collapsed due to flooding, preventing freight transport on the Dovrebanen. The bridge was reopened in May 2024.

Domestic civil aviation was greatly affected by the travel restrictions enforced due to COVID-19. These were partly still in place in beginning of 2022. The subsequent increase in price levels and cost of living, higher interest rates and geopolitical unrest have resulted in people travelling less by plane compared to 2019. The overall number of passengers was down 10 per cent in 2023 compared to pre-Covid levels. The travel pattern has also changed. There are fewer business travellers than before, and domestic travel activity has flattened. There is however an increasing trend in international air passengers (mainly from increased tourism) in the domestic market. As a result of this greenhouse gas emissions from domestic civil aviation (including helicopters) are still slightly below 2019 levels.

Industrial processes and product use (IPPU)

A considerable part of Norwegian manufacturing industries is based on natural resources. The historic availability of low-cost hydro power created a basis for the establishment of metal and fertilizer production. Some chemical production is based on the petroleum resources. Production of pulp and paper derived from the forest resources has also been considerable, and the fisheries have also given a base for industry. Norwegian industry therefore has a high share of production of raw materials and semi-manufactured goods including iron and steel, non-ferrous metals, chemicals, fertilisers, pulp and paper, mineral industries, food processing industries, building and construction industry.

The emissions from the IPPU sector were at about 19 per cent of the national totals in 2022. The emissions have decreased by 37 per cent from 1990.

Waste

The waste sector, with emissions of 1.4 million tonnes of CO2 equivalents in 2022, accounted for 2.9 per cent of the national GHG emissions. Most of the emissions from the waste sector originate from solid waste disposal on land (61 per cent).

Economic growth, or growth in production and consumption, is the key driver behind the growing waste volume. Even though the total amount of waste generated has increased, GHG emissions from the waste sector have generally decreased since 1990. This is due to the increase in material recycling and the ban issued in 2009 on disposing biodegradable waste to landfill. The central government authorities set the general framework, while municipalities and industry are responsible for waste collection and treatment.

In general, targets set in EU waste directives, such as EU targets for preparing for reuse and recycling of municipal waste, also apply for Norway owing to the EEA agreement.

Agriculture

Stretched along the western side of the Scandinavian Peninsula, approximately one fourth of the surface area of Norway lies north of the Arctic Circle. The long coastline has an Atlantic, humid climate, while the inland climate is continental. Approximately 3 per cent of Norway’s land area is cultivated soil. The most suitable lands, approximately 1 per cent, is mostly allocated to arable crops, while grassland and ruminant livestock are allocated to regions less suitable for arable crops. While cultivated soil is a scarce resource in Norway, in addition we have extensive pastureland that is used extensively by reindeer husbandry and summer pasture for other ruminant livestock.

Agriculture is estimated to account for about 9.5 per cent of Norway’s emissions of greenhouse gases in 2022. This particularly includes methane and nitrous oxide from animal husbandry and fertilisation. In addition, nitrous oxide emissions from cultivation of peatland are allocated to agriculture, while CO2 emissions from the same source are allocated to LULUCF. Use of fossil fuels for agricultural activities are allocated to other sectors, e.g. transport. The agricultural emissions have been reduced by approximately 6.8 per cent since 1990.

2.1.2.1 Land use, land-use change and forestry (LULUCF)

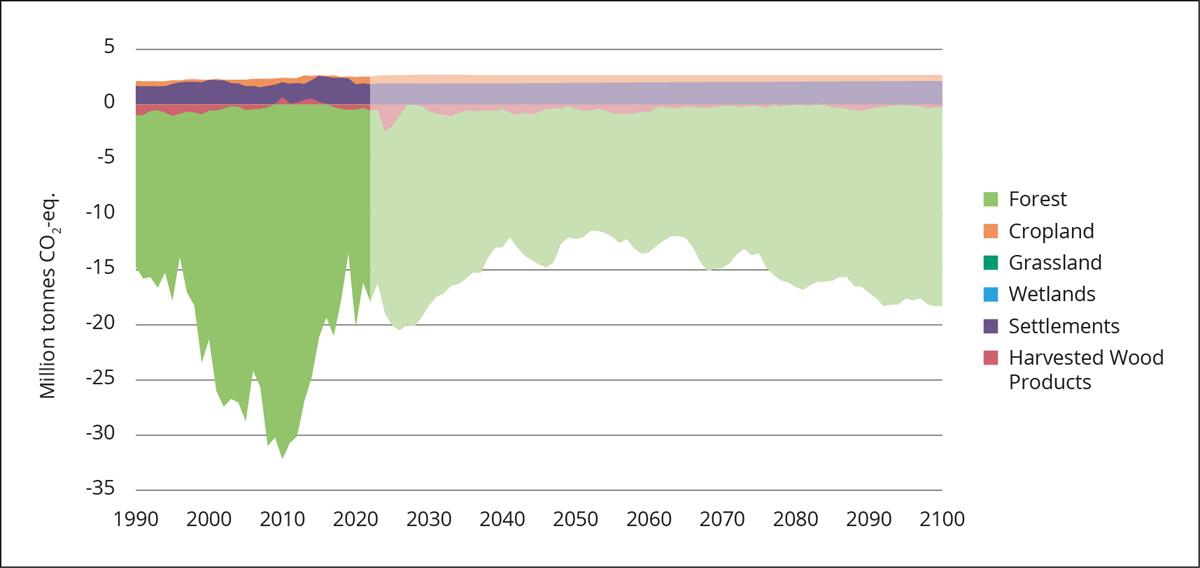

Forest and wooded land cover about 12 million hectares and constitute approximately 38 per cent of the land area in Norway. Approximately 88 per cent – that is 120,000 properties – of the forest area is privately owned. The majority of the forest holdings are farm and family forests. Grassland has the second largest area covering as much as 35 per cent of the mainland, with the vast majority categorized as extensive grasslands.

Net land-use changes in Norway from 1990 to 2022 are small compared to the total area. Overall, the area of settlements has increased from 1.8 per cent of the total area in 1990 to 2.2 per cent in 2022. Forest land, grasslands, and wetlands have shown a slight decline in area, while cropland and other land have remained more or less constant.

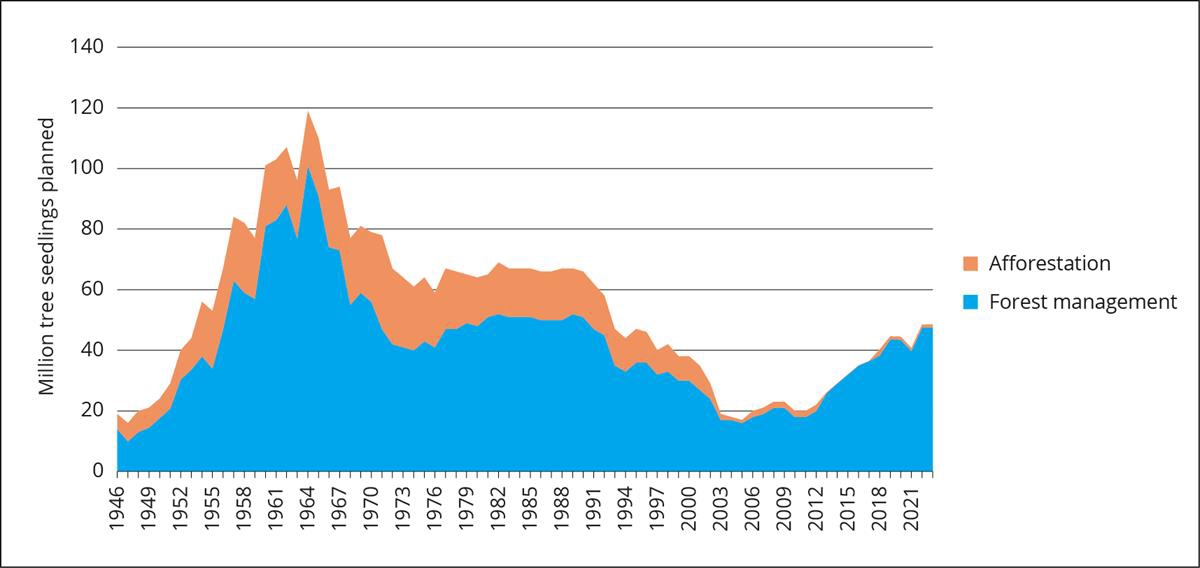

The most widespread species are Norway spruce (47 per cent), Scots pine (33 per cent) and birch (18 per cent). The historical levels of tree planting in the Norwegian forestry are shown in Figure 2.5. Norway spruce (picea abies) and Scots pine account for more than 95 per cent of the seedlings. Broadleaves and foreign tree species are only planted to a small extent.

From 1990 to 2010, both carbon sequestration and emissions in the LULUCF sector increased, while the net carbon sequestration declined from 2011 to 2022. In 2022, net sequestration in the sector was estimated at 13.8 million tonnes of CO2 equivalents, equivalent to 28 per cent of Norway’s total greenhouse gas emissions. Forests are the primary source of carbon sequestration, accounting for 17.9 million tonnes of CO2 equivalents in 2022, compared to 14.7 million tonnes in 1990. Due to methodological changes after UN revisions, the LULUCF removals are significantly lower (approximately 6.5 million tonnes ) than in Norway`s 8th National Communication. Post-war forest planting has played an important role in this sequestration. However, the decline in sequestration since 2010 has been driven by drought in 2018 with delayed recovery, increased logging, a rise in the proportion of mature forests with slower growth rates, and reduced forest planting and silvicultural activities in recent decades.

Emissions from deforestation, associated with land-use change from forest to other land categories (e.g., agriculture and urban development), increased from 2.1 million tonnes in 1990 to 2.5 million tonnes of CO2 equivalents in 2022. Emissions from settlements contribute to yearly emissions of about 1.9 million tonnes, and these emissions are projected to remain stable towards 2050.

Figur 2.5 Historical levels of tree planting in the Norwegian forestry

Source: Ministry of Agriculture and Food

2.1.3 Institutional arrangements

The overall national climate policy is decided by the Storting (Norwegian Parliament), and the government implements and administers the most important policies and measures, such as economic instruments and direct regulations. Most policies and measures in the area of climate policy are developed through interministerial processes before the political proposals are tabled. The Ministry of Climate and Environment has the overarching responsibility for coordinating climate efforts and reporting on the overall achievement of climate goals. The Ministry of Finance is responsible for the tax schemes. The other ministries are responsible for policies in their respective sectors. The Ministry of Climate and Environment organizes the work of developing and further refining the decision-making basis through a climate governance system.

Norway has several legislative arrangements in place in order to help reduce emissions of greenhouse gases, such as the Pollution Control Act, the Greenhouse Gas Emissions Trading Act, the CO2 Tax Act, and the Petroleum Act, as well as requirements under the Planning and Building Act. The relevant arrangements will be discussed in more detail in chapter 2.5.

The Climate Change Act

In June 2017, the Norwegian Parliament adopted the Climate Change Act, which establishes by law Norway’s emission reduction targets for 2030 and 2050. The purpose of the act is to promote the long-term transformation of Norway in a climate-friendly direction. See further description of Norway’s climate targets in 2.2.

The act has an overarching function in addition to existing environmental legislation. The Climate Change Act introduces a system of five year reviews of Norway’s climate targets, on the same principle as the Paris Agreement. In addition, the act introduces an annual reporting mechanism. The Government shall each year submit to the Parliament updated information on status and progress in achieving the climate targets under the law, and how Norway prepares for and adapts to climate change. Information on the expected effects of the proposed budget on greenhouse gas emissions and projections of emissions and removals are also compulsory elements of the annual reporting mechanism. Since 2018, the Government has annually reported information as required by the Climate Change Act as part of the state budget process in October each year. Since 2022, the reporting has been submitted to the Storting as sperate annex to the state budget named Climate Status and Plan, which is further explained in Box 2.1 in chapter 2.3.

On 1 October the Government issued on a public consultation a proposal for a new climate target for 2035 to be included in the Norwegian Climate Change Act9. The consultation ends 1 January 2025. After the consultation the Government will send a concrete proposal to the Parliament for approval and adoption.

Climate Governance System

In addition to complying with the reporting mechanism of the Climate Change Act, the Government’s Climate Status and Plan presented a Climate Governance System in 2022. The purpose of the climate governance system is to facilitate the achievement of Norway’s climate goals. The system aims to provide processes for improved coordination for informed decisions, implementation, and reporting. It establishes annual routines and milestones for the design, follow-up, and reporting, as well as milestones for further development of climate policies. Some decision-making milestones are coordinated with the Government’s internal budgetary processes, enabling budgetary decisions as well as decisions on other climate policies to be informed by their estimated effect on emissions and the achievement of climate targets. The government’s annual Climate Status and Plan and regular white papers to the Storting present updates on climate policy developments and plans as well as progress towards meeting climate goals. Policies developed for purposes other than climate mitigation but still affecting greenhouse emissions are developed across sectors and presented in different white papers, action plans, and strategies. The system is being developed further.

Institutional arrangements related to cooperation with the EU

Norway intends to fulfil its climate target (Nationally Determined Contribution) for 2030 under the Paris Agreement in cooperation with the EU. The Emissions Trading System is a part of the EEA agreement. This cooperation will be reflected through transfers and acquisitions of ITMOs pursuant to Article 6 of the Paris Agreement. Details of the cooperation including the institutional arrangements for Article 6 will be reported in a forthcoming Initial Report pursuant to Decisions 2/CMA. 3 and 6/CMA. 4. The Ministry for Climate and Environment has however established arrangements for acquisition of units under the pillars ESR and LULUCF in the cooperation with EU, as well as a program for acquisition of ITMOs, both pursuant to allotments in the state budget.10 These programs are expected to acquire ITMOs and can be drawn upon in case domestic measures and cooperation with the EU does not lead to a full realisation of emission/removal budgets under the cooperation with EU and/or the cooperation does not fully realize Norway’s climate target in the NDC for 2030.

Local governments

Local governments are responsible for implementing policies and measures at the local level, for example through waste management, spatial and societal planning and some transport measures. In 2009, central government planning guidelines (Nw. statlige planretningslinjer) for climate and energy planning were introduced in municipalities. Since 2018, these guidelines also include a description of how municipalities and counties can incorporate climate adaptation work into their planning activities. The government is in the process of revising the guidelines, with the goal of clarifying expectations for municipalities’ ambitions and results in energy and climate work. The work is now in its final phase, and the new guideline is expected to be finished in the beginning of 2025.

Public participation

The Environmental Information Act, implementing the Aarhus Convention, establishes public participation in decision making processes relevant for the environment. For example, the Climate Change Act was on a public hearing including all stakeholders. All plans made in accordance with the Planning and Building Act must also be subject to public participation.

The Norwegian Environment Agency

The Norwegian Environment Agency is a government agency under the Ministry of Climate and Environment. The Environment Agency implements government pollution and nature management policy. Important fields of work in relation to pollution control include climate, hazardous substances, water and the marine environment, waste management, air quality and noise. The Environment Agency manages and enforces the Pollution Control Act, the Product Control Act and the Greenhouse Gas Emission Trading Act, and the Nature Diversity Act, among others. The Environment Agency grants pollution permits, establishes requirements and sets emission limits, and carries out inspections to ensure compliance.

The Norwegian Environment Agency provides analyses and impact assessments related to environmental policies and measures. One example is an annual mitigation analysis on climate, which informs the government and the public on possible mitigation actions to reduce Norwegian greenhouse gas emissions.11

The Environment Agency monitors the state of the environment. The Agency provide environmental information to the public through their home page.12 The Agency also informs about Norway’s climate and environmental goals.13

The Environment Agency supervises and monitors the County Governors’ work on pollution, coordinates the County Governors’ inspection work and organises joint inspections. The Environment Agency provides guidelines for the County Governors and also deals with appeals against decisions made by the County Governors.

The Environment Agency participates in a series of international processes, to promote regional and global agreements that reduce serious environmental problems. Moreover, the Environment Agency also cooperates with the environmental authorities in other countries, sharing competence and furthering environmental improvements.

The Norwegian Environment Agency is appointed as a national entity with overall responsibility for the GHG inventory and the reporting of the inventory. The GHG inventory is produced and reported in collaboration with Statistics Norway and the Norwegian Institute of Bioeconomy Research. The three institutions are responsible for archiving necessary documentation.

There have not been any significant changes to the institutional arrangements since Norway reported its 8th National Communication in 2022.

2.2 Norway’s climate policy and targets

Norway’s climate policy is based on the objective of the United Nations Framework Convention on Climate Change and the Paris Agreement. The scientific understanding of the greenhouse effect set out in the reports from IPCC is an important factor in developing climate policy. Thus, the policies and measures reported are seen as modifying long-term trends in anthropogenic greenhouse gas emissions and removals.

Climate change and emissions of greenhouse gases have featured on the policy agenda in Norway since the late 1980s. Today, Norway has a comprehensive set of measures covering almost all emissions of greenhouse gases as well as removals.

Norway has ambitious climate targets, both under the Paris Agreement and within a domestic context, forming a basis for the policies and measures:

Paris Agreement NDC

The nationally determined contribution (NDC) is to reduce emissions by at least 55 per cent by 2030 compared to 1990. The NDC target is included in the Norwegian Climate Change Act.

On 1st October 2024 the Government issued a proposal for a new climate target for 2035 to be included in the Norwegian Climate Change Act for public consultation until 1st January 2025. After the consultation the Government will send a concrete proposal to the Parliament for approval and adoption. After the Parliamentary approval Norway will submit its target as its new NDC under the Paris Agreement.

Targets in a domestic context

Become a low-emission society by 2050 and reduce emissions by 90–95 per cent compared to 1990. The effect of Norway’s participation in the EU Emissions Trading System is to be taken into account in assessing progress towards this target. The target is included in the Norwegian Climate Change Act.

As an interim goal on the road to net zero emissions and the low-emission society, the government has set a transition target for the entire economy in 2030. This is formulated in the government platform as a target to cut Norwegian emissions by 55 per cent compared to 1990.

Be climate neutral from 2030.

2.3 Description of Norway’s NDC for 2030

This chapter of the BTR describes Norway’s NDC under Article 4 of the Paris Agreement against which progress will be tracked. Following the decision 1/CMA.3 Glasgow Climate Pact paragraph 29, Norway revisited the 2030 target in its Nationally Determined Contribution (NDC). In November 2022, Norway communicated its updated NDC to reduce emissions by at least 55 per cent by 2030, compared to 1990 levels.14

Details of Norway’s NDC are shown in Table 2.2. The NDC is economy wide and is a single-year target in 2030. It covers the gases carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), perfluorocarbons (PFCs), hydrofluorocarbons (HFCs), sulphur hexafluoride (SF6) and nitrogen trifluoride (NF3)15. The NDC covers all the sectors in the GHG inventory. Emissions and removals from the LULUCF sector that are additional will be accounted for when assessing achievement of the target.

Norway’s intention is to fulfil this target in cooperation with the EU. This will be done within the framework set up by Article 6 of the Paris Agreement. In the event that the cooperation with the EU does not lead to a full realization of the target, Norway intends to use ITMOs acquired from countries outside the EEA.

Tabell 2.2 Description of a Party’s nationally determined contribution under Article 4 of the Paris Agreement, including updates

Description

Target(s) and description, including target type(s), as applicable

Economy-wide, emission reductions by at least 55 per cent in 2030 compared to base year (1990) emissions.

Target year(s) or period(s), and whether they are single-year or multi-year target(s), as applicable

Single-year target in 2030.

Reference point(s), level(s), baseline(s), base year(s) or starting point(s), and their respective value(s), as applicable

Base year: 1990. Base year value: 51 263.14 kt tonnes CO2 equivalents

Time frame(s) and/or periods for implementation, as applicable

From 1st January 2021- 31st December 2030.

Scope and coverage, including, as relevant, sectors, categories, activities, sources and sinks, pools and gases, as applicable

Sectors: Energy, industrial processes and product use, agriculture, land-use, land-use change and forestry, and waste.

For the land-use, land-use change and forestry sector, emissions and removals the following reporting categories are included: forest land, cropland, grassland, and wetland (wetland remaining wetland only from 2026), including land use changes between the categories, and between these categories and settlements and other land. The five carbon pools above-ground biomass, below-ground biomass, litter, dead wood and soil organic matters are included. In addition, the carbon pool harvested wood products is included.

Emissions and removals from the LULUCF sector that are additional will be accounted for when assessing achievement of the target, see chapter 2.3 for further details.

Intention to use cooperative approaches that involve the use of ITMOs under Article 6 towards NDCs under Article 4 of the Paris Agreement, as applicable

Yes. Norway pursues cooperation with the EU on implementing the respective NDCs to be reflected in accordance with rules under Article 6 of the Paris Agreement. If the cooperation with the European union does not fully realize the NDC target, Norway will use voluntary cooperaton cooperation with countries outside the European Economic Area to fulfil the part of the NDC that goes beyond what is achieved with the European Union. See chapter 2.3 of this BTR for details .

Any updates or clarifications of previously reported information, as applicable

Norway will report on its choice of accounting method for cooperative approaches in its forthcoming Initial Report pursuant to the rules under Article 6 in Decision 2/CMA.3.

EU and Norway need to agree on how to account for the reductions achieved in the common Emissions Trading System (such an agreement was made pursuant to the unit flow under the Kyoto Protocol) and rules pertaining to any flows of ITMOs reflecting flows of units under other pillars of the cooperation.

Iceland and Norway entered into an agreement with the EU in October 2019 to cooperate to fulfil their respective climate targets for 2030. Under the agreement, Norway will take part in EU climate legislation from 2021 to 2030. Final accounting towards the target pursuant to the guidance under Article 6.2 may depend on any further arrangements in Norway’s cooperation with the EU and Iceland, in particular resulting from participation in the European Emissions Trading System. Norwegian entities have undertaken and is expected to further undertake a net purchase of allowances in the ETS in the current NDC period. This net purchase will be reflected in a net acquisition of ITMOs to be accounted towards the NDC. Further specification of accounting method is to be developed by Norway and EU in accordance with rules set up by the CMA in Glasgow in 2021 so as to avoid double counting. If necessary, Norway will use voluntary cooperation with countries outside the EEA under Article 6 of the Paris Agreement to fulfil any part that goes beyond what is achieved through the climate cooperation with the European Union. Norway has established a purchase program for ITMOs from developing countries that could be used in such an event.16 The program is allotted NOK 8.2 billion through the state budget. An agreement is signed with Uzbekistan through the World Bank program Transitional Carbon Asset Facility (TCAF), and initial MoUs or agreements are developed with Benin, Indonesia, Jordan, Morocco, Senegal and Zambia for cooperation facilitated by the Global Green Growth Institute.

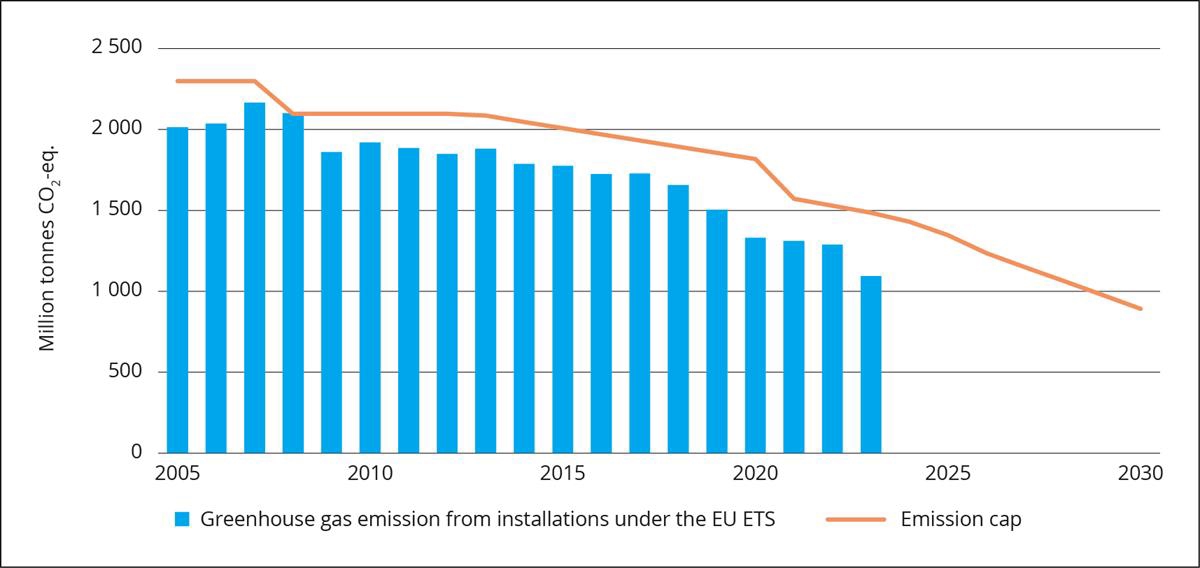

The EU’s climate policy has three main pillars. The first pillar of EU climate policy deals with ETS emissions. The EU Emissions Trading System applies to the largest emission sources within Norwegian manufacturing industries and the petroleum industry through the European Economic Area (EEA). The cap, or number of emission allowances in the system, is being gradually reduced to achieve a reduction of 62 per cent in emissions in 2030 compared with 2005. This is an overall reduction for all installations covered by the EU ETS. Emissions from European aviation have been included in the EU ETS since 2012, while emissions from maritime transport are gradually included from 2024.

The second pillar of EU climate policy deals with emissions not covered by the EU ETS, but by the effort sharing regulation (ESR) mainly covering emissions from transport, agriculture, buildings and waste. Norway’s current target for the ESR emissions under its agreement with the EU is a 40 per cent reduction by 2030 compared with the 2005 level. This has been translated into a binding emission budget with emission ceilings for each year in the period 2021–2030. The legislation allows for each country’s emission budget to be met through a combination of emission reductions within the country and transfers of emission units from other EU countries.

The third pillar of EU climate policy deals with the Land Use, Land Use Change and Forestry (LULUCF) sector. This includes anthropogenic emissions and removals of greenhouse gases from land use, land use change and forestry. The factors that particularly influence emissions and removals are growth, mortality and the level of harvesting (relative to harvest level modelled in the forest reference level FRL (2021–2025, or reference period (2026–2030)), land-use change such as deforestation and afforestation, and the natural spread of forest and scrub. The EU’s climate legislation includes accounting rules for emissions and removals in the LULUCF sector. However, neither Norway nor EU are applying these rules for accounting contributions from LULUCF towards the NDC. Under the EU legislation, Norway currently has an obligation to ensure that overall greenhouse gas emissions from the LULUCF sector do not exceed removals (this is known as the ‘no debit’ rule). According to the regulation, the obligation can be fulfilled by implementing measures in the national LULUCF sector, and/or through extra national reductions in non-ETS emissions, for example in the transport and agriculture sectors, and/or through purchasing units from EU countries or Iceland.

When Norway and the EU concluded their agreement on implementing the EU legislation on ESR and LULUCF, the targets each of these parties had communicated to the UN was a 40 per cent reduction in emissions by 2030 compared with the 1990 level. Both the EU and Norway have communicated more ambitious targets to the UN after the conclusion of the agreement, and the EU has adopted amendments to its legislation in order to ensure that the more ambitious target is achieved. Norway is considering whether the updated EU legislation on ESR and LULUCF should also be made applicable in Norway, and if so on what conditions. The updated legislation will not apply to Norway until the Storting has given its consent.

Norway is not mentioned in the referenced updated EU legislation. Based on the targets for ESR emissions that apply for comparable countries, it is likely that Norway can get a reduction target of 50 per cent reduction compared to 2005 should the climate agreement with the EU be updated. Such a target will be translated into a binding emission budget with emission ceilings for each year in the period 2021–2030. For information on the climate status and plan for the 2030 climate target where assumed targets are pursued, see Box 2.1.

Boks 2.1 Annual Climate Status and Plan

The Climate Status and Plan summarises the government’s climate policy, and it is the government’s annual report on the information required by the Climate Change Act. The Støre Government presented an updated Climate Status and Plan in a separate attachment to Prop. 1 S (2024–2025) in October 2024.

Since Norway and the EU both have individual NDCs/targets under the Paris Agreement, the cooperation is envisaged to include transfers and acquisitions of ITMOs and follow the guidance under Article 6 of the Paris Agreement. See Box 2.2 for further information.

ESR emissions

Chapter 2.7 of this BTR presents updated projections of GHG emissions. Table 2.8 shows that the projections for the ESR emissions are estimated to decrease from 25.2 million tonnes CO2 eq. in 2022 to 19.8 million tonnes CO2 eq. in 2030. The projections for the period 2021–2030 are about 13 million tonnes CO2 eq. higher than the given emission budget under the current EU legislation for the ESR sector (40 per cent reduction in 2030 compared to 2005).

Correspondingly, the emissions are about 22 million tonnes CO2 eq. higher than the estimated emission budget Norway may get, should the climate agreement with the EU be updated and Norway gets a reduction target of 50 per cent compared to 2005, based on the proposal from the EU Commission. The Støre-government is therefore making provisions for, and is planning to, reduce the ESR emissions by 50 per cent by 2030.

In the budget proposal for 2025 and the attached Climate Status and Plan, the Støre-government proposes climate measures that can reduce the GHG emissions. It is estimated that measures proposed in the Climate Status and Plan can reduce the non-ETS emissions by 16.5 million tonnes of CO2 eq. in the period 2021–2030. The planned measures are reported as projections with additional measures (WAM), see chapter 2.5.11 and chapter 2.7.6 for further information.

With these measures the total estimated ESR emissions for the period 2021–2030 would be about 2.8 million less than the emission budget under the current EU legislation for the ESR sector (40 per cent reduction in 2030 compared to 2005). Estimated emissions including planned measures for the period 2021–2030 would be 5.4 million higher than the estimated emission budget Norway may get should the climate agreement with the EU be updated and Norway gets a reduction target of 50 per cent compared to 2005. For the year of 2030, estimated emission reductions including planned measures are about 46 per cent compared to 2005-levels.

Box 2.1 continued

Based on these projections, Norway is expecting to have to use flexible mechanisms in addition to national measures to meet the commitment over the period 2021–2030. Norway has access to approximately 5.8 million converted allowances from the EU ETS, which can be used under ERS and land-use regulations. The government has set aside funds for utilisation of further flexibility if needed through acquisition of units from other counties. However, the availability of units under both the ESR and the LULUCF from EU countries is unknown, as well as the price.

Boks 2.2 Pursuing cooperation with the EU on implementing the respective NDCs

Norway pursues cooperation with the EU on implementing their respective NDCs. Norway, Iceland and Liechtenstein have been participating in the EU ETS since 2008. For the period from 1st January 2021 to 31st December 2030, Norway is pursuing its cooperation with the EU on implementing their respective NDCs and have together with Iceland agreed to implement the EU Effort Sharing Regulation (ESR) and LULUCF Regulation in accordance with the EEA Agreement Protocol 31.

Cooperation on implementation of the NDC enables Norway to have a higher level of ambition and thus gives a benefit to the atmosphere. In 2019, the EU, Iceland and Norway agreed on cooperation to fulfil our respective prevailing NDCs. Since then, the EU, Iceland and Norway have updated their respective NDCs and strengthened the targets substantially. The conditions for Norwegian participation in the updated European legislation (Effort Sharing Regulation and LULUCF Regulation) will need to be agreed between EU and Norway before arrangements related to cooperative approaches pursuant to Article 6 of the Paris Agreement on implementation of the updated NDCs can be finalised.

Details concerning the possible flow of internationally transferred mitigation outcomes (ITMOs), accounting approaches, national arrangements, registries, other reporting requirements including related to adaptation finance and overall mitigation of global emissions, will be addressed in future reporting under the Paris Agreement, in particular the Initial Report pursuant to the Article 6 guidance.

2.4 Information necessary to track progress made in implementing and achieving Norway’s NDC

Norway’s point of departure for accounting and showing progress towards the NDC target is the inventory figures. Voluntary cooperation with other countries, and subsequent accounting for ITMOs received, is a central element in the implementation of the NDC. There will be several years’ delay in the transfer of ITMOs reflecting the underlying cooperative approaches with EU and potentially other countries outside of the European Economic Area.

Norway expects that the net flow of allowances between EU and Norway in the European ETS will be the basis for transfer of ITMOs also under the Paris Agreement, as was the case under the Kyoto Protocol. Further details defining such net flow is to be agreed between the parties. However, Norwegian companies have acquired and used significantly more allowances in the ETS than we expect that Norway will be held responsible for under this cooperative approach, which will then lead to a significant transfer of ITMOs from EU to Norway. Under the Kyoto Protocol such transfers closed most of the gap between the actual Norwegian emissions and the commitments in both periods; see the final compilation and accounting reports17. The remaining gap was closed using units from the Clean Development Mechanism and also some from Joint Implementation.

Norway, as well as the EU and other cooperating partner countries, will have to submit our respective Initial Reports pursuant to Decision 2/CMA. 3 (and 6/CMA.4 and X/CMA.6) to spell out further details around the accounting.

2.4.1 Indicator, methodologies and structured summary

This section of the BTR contains information in accordance with paragraphs 65–77 and 79 of the MPGs. The information is also reported in CTF tables 1 to 4.

2.4.1.1 Indicator for tracking progress

Norway has selected the indicator «emissions without LULUCF» as the indicator representing the point of departure in tracking progress towards the implementation and achievement of Norway’s NDC. The unit and metric are the same as the NDC’s base year value and target value. Tables 2.3 and 2.4 provide more information on this indicator. Additional emissions and removals from the LULUCF sector and ITMOs acquired under Article 6 of the Paris agreement will add clarity on the progress towards the 2030 target and will be reported in future BTRs.

Total CO2 equivalent emissions, including indirect CO2, without LULUCF.

Information for the reference point(s), level(s), baseline(s), base year(s) or starting point(s), as appropriate

The reference level is the total CO2 equivalent emissions, including indirect CO2, without LULUCF reported for the base year 1990. The reference level for Norway is 51 263.14 kt tonnes CO2 equivalents.

Updates in accordance with any recalculation of the GHG inventory, as appropriateb

This is the first time the reference level is reported in accordance with the MPGs, hence there are no updates. The value of the reference level has been recalculated since Norway updated its NDC and may be updated in the future due to methodological improvements to the GHG inventory.

Relation to NDCc

The indicator is defined in the same unit and metric as the target of the NDC.

The total is reported in the CRT tables of Norway’s GHG inventory. The relevant total is «Total CO2 equivalent emissions, including indirect CO2, without LULUCF».

Any sector or category defined differently than in the national inventory report:

4. Land use, land-use change and forestry

For the LULUCF sector, only a subset of emissions and removals are included through them being identified as additional removals and emissions. There is ongoing work to clarify this method.

Definition needed to understand mitigation co-benefits of adaptation actions and/or economic diversification plans:

Adaptation actions

Not applicable

Economic diversification plans

Not applicable

Any other relevant definitions

NA

For the emissions and removals from the LULUCF sector, additional emissions and removals in this sector will be accounted for towards the target.

Norway expects that the cooperation with the EU will be reflected through transfer of ITMOs based on net flow of allowances between EU and Norway in the ETS and possibly any flows of units under the pillars ESR and LULUCF. In the event that this cooperation does not fully realize the NDC target of at least 55, Norway will also use ITMOs acquired from countries outside the European Economic Area through its purchase program.

2.4.1.2 Methodologies and accounting approach

Norway will use the following accounting approach for tracking progress towards its NDC: Annual total CO2 equivalent emissions, including indirect CO2, without LULUCF are compared to the economy-wide absolute emission reduction as defined in the NDC.

For the emissions and removals from the LULUCF sector, the Government has not yet identified the concrete method that will be used to account for the additional emissions and removals. There is ongoing work to clarify this method.

The figures reflecting GHG emissions are then adjusted for any net transfers of ITMOs between Norway and the EU and between Norway other Parties. Norway’s emissions balance would reflect the level of emissions and removals covered by its NDCs and adjusted using corresponding adjustments.

Details on methodologies and accounting approaches consistent with the accounting guidance18 under the Paris Agreement can be found in CTF table 3 (‘Methodologies and accounting approaches’), which has been submitted electronically together with this BTR.

The national GHG inventory represents the starting point for accounting towards the 2030 single year target. Norway will also cooperate with other countries under Article 6; notably cooperation with the EU under Article 6.2, but also cooperation with other countries.

Norway will report on how it will account for the use of ITMOs towards its single year 2030 target in a forthcoming Initial Report pursuant to Decisions 2/CMA.3 and 6/CMA.4. Given that the pillars in the cooperation with the EU form budgets that can be seen as trajectories towards emissions levels in the target year, Norway sees the possibility of using a trajectory or trajectories in accordance with the guidance in decision 2/CMA.3 Annex para 7 a i. The pillars in the EU legislation are designed to realize an overall reduction of at least 55 per cent in 2030. EU and Norway have individual NDCs with single year targets individually accounted for. For Norway implementing the requirements under the pillars and reflecting ITMO flows through an Article 6.2 cooperative approach may, however, not ensure that Norway fully realizes a reduction of 55 per cent.

Figur 2.6 Greenhouse gas emissions and cap in the EU emission trading scheme (EU ETS)

Source: Ministry of Climate and Environment

Tabell 2.5 The Norwegian budget for ESR emissions (million tonnes CO2 equivalents)

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2021-2030

ESR Budget 50 per cent reduction

25.2

24.3

23.1

21.8

20.6

21.2

19.5

17.8

16.1

14.5

204.1

Actual GHG emissions

25.5

25.2

24.1

-

-

-

-

-

-

-

226.0

Projected GHG emissions

23.5

22.8

22.2

21.7

21.1

20.2

19.6

Gap – 50 per cent reduction

0.3

0.9

1.1

1.7

2.2

1.1

2.2

3.3

4.1

5.1

21.9

In the calculation of the emissions gap, it is assumed that the EU will allow the accounting of negative emissions from carbon capture and storage under the effort sharing. If the EU does not allow this, the emissions gap will increase by approximately 0.7 million tonnes of CO2 equivalents.

Source: Government’s Climate Status and Plan for 202519

For the ETS there is one trajectory common for all of the EEA trading partners. This trajectory will reduce the cap – the annual volume of allowances – by 62 per cent compared to 2005 levels in 2030. If we were to apply the trajectory of the overall cap to Norway, its emissions from stationary sectors included in the system would be reduced to about 10 Mt in 2030. It is expected that Norway and the EU will develop rules guiding transfers of ITMOs pursuant the net flow of EUAs acquired and used in the ETS. Such an arrangement was already made under the Kyoto Protocol for 2008–2012 and 2013–2020, see documentation here; Norway’s multilateral assessment | UNFCCC; in particular chapter 4.5 in Norway’s fifth biennial report and relevant review reports.

The emission reduction target for Norway under the Effort Sharing Regulation (ESR) is expected to be a 50 per cent reduction in 2030, also compared to 2005 levels. The resulting emissions level would be 14.5 Mt in 2030, see Table 2.5. If the ESR trajectory is not fully realized through domestic emissions reductions as reflected in the inventory and other forms of flexibility (use of EUAs), there will be a need to acquire units from EU/EEA countries. It is envisaged that any net transfer of such units would be mirrored by transfers of ITMOs.

The trajectories for ETS plus ESR would result in a level of 24.5 Mt in 2030, corresponding to a reduction of 52.5 per cent.

Further, Norway will account additional domestic emissions and removals from the LULUCF-sector towards the target. Any net transfer or acquisition of LULUCF units within the EU/EEA cooperation may also be reflected as ITMO transfers and could thus be accounted for towards the target, subject to agreement with the EU on the matter.

2.4.1.3 Structured summary, status of progress

The key information for tracking progress towards achieving the NDC target is the most recent information on GHG emissions and removals in the scope of the NDC. Table 2.6 (CTF table 4 Tracking progress made in implementing and achieving the NDC under Article 4 of the Paris Agreement) summarises the current status of progress.

Tabell 2.6 (CTF table 4) Structured summary: Tracking progress made in implementing and achieving the NDC under Article 4 of the Paris Agreement

Unit, as applicable

Reference point(s), level(s), baseline(s), base year(s) or starting point(s), as appropriate (paras. 67 and 77(a)(i) of the MPGs)

Implementation period of the NDC covering information for previous reporting years, as applicable, and the most recent year, including the end year or end of period (paras. 68 and 77(a)(ii–iii) of the MPGs)

Target levelb

Target year or period

Progress made towards the NDC, as determined by comparing the most recent information for each selected indicator, including for the end year or end of period, with the reference point(s), level(s), baseline(s), base year(s) or starting point(s) (paras. 69–70 of the MPGs)

1990

2021

2022

Indicator(s) selected to track progress of the NDC or portion of NDC under Article 4 of the Paris Agreement (paras. 65 and 77(a) of the MPGs):

Emissions without LULUCF

kt CO2 equivalent

51 263.14

49 254.43

48 879.49

23 068.41

2030

The most recent level of the indicator reported in the NIR is 4.7 per cemt below the base year level. Preliminary estimate for 2023 is 9.1 per cent lower than in the base year. Information on ITMOs pursuant to Article 6 cooperative approaches will be submitted in future BTRs when such approaches have been agreed between Norway and other parties.

Where applicable, total GHG emissions and removals consistent with the coverage of the NDC (para. 77(b) of the MPGs)

kt CO2 equivalent

49 254.43

48 879.49

Contribution from the LULUCF sector for each year of the target period or target year, if not included in the inventory time series of total net GHG emissions and removals, as applicable (para. 77(c) of the MPGs)

kt CO2 equivalent

NE

NE

Each Party that participates in cooperative approaches that involve the use of ITMOs towards an NDC under Article 4 of the Paris Agreement, or authorizes the use of mitigation outcomes for international mitigation purposes other than achievement of the NDC, shall provide (para. 77(d) of the MPGs):

NA

NA

Information on ITMOs pursuant to Article 6 cooperative approaches will be submitted in future BTRs when such approaches have been agreed between Norway and other parties, where the largest volume is expected to reflect cooperation with the EU on the ETS. For this BTR1, there is not yet any information to report in this table.

It is a priority for Norway to clarify the method for identifying additional removals and emissions from the LULUCF-sector, both for planning purposes and to reflect the contribution fully in future BTRs. Since the methodology to document additional emissions and removals in the LULUCF sector is not yet developed, the contribution from the LULUCF sector is reported as not estimated (NE) in the years 2021 and 2022.

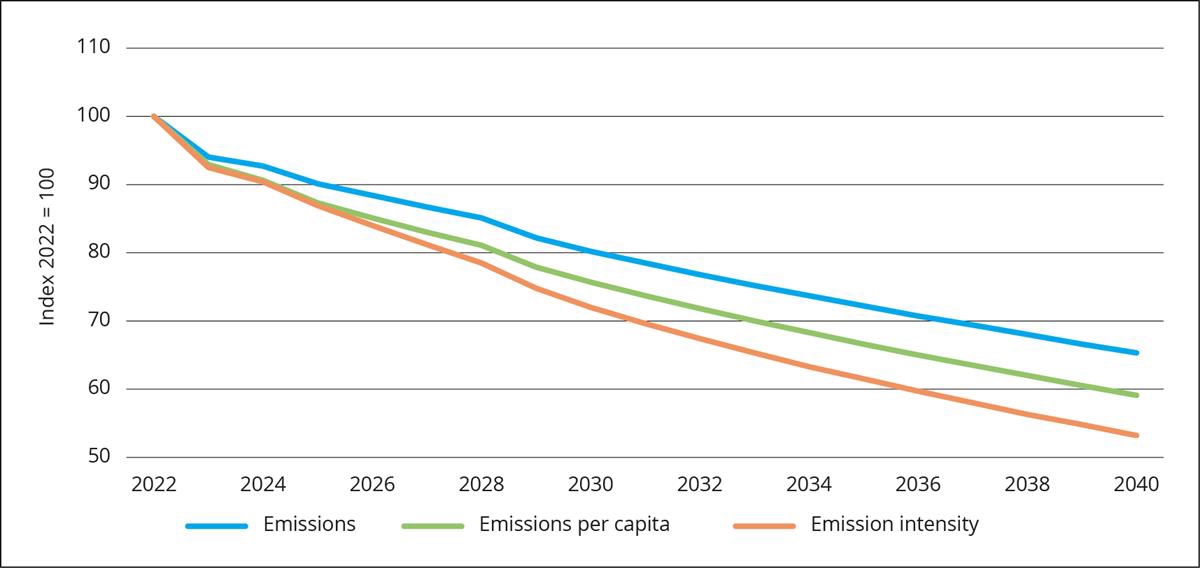

Based on Norway’s GHG inventory data, the emissions without LULUCF in 2022 were 4.7 per cent lower than the base year emissions in 1990. Preliminary estimates of the emissions in 2023 that have not yet been reported to the UNFCCC indicate that the emissions without LULUCF have decreased further and were 9.1 per cent lower than in 1990.

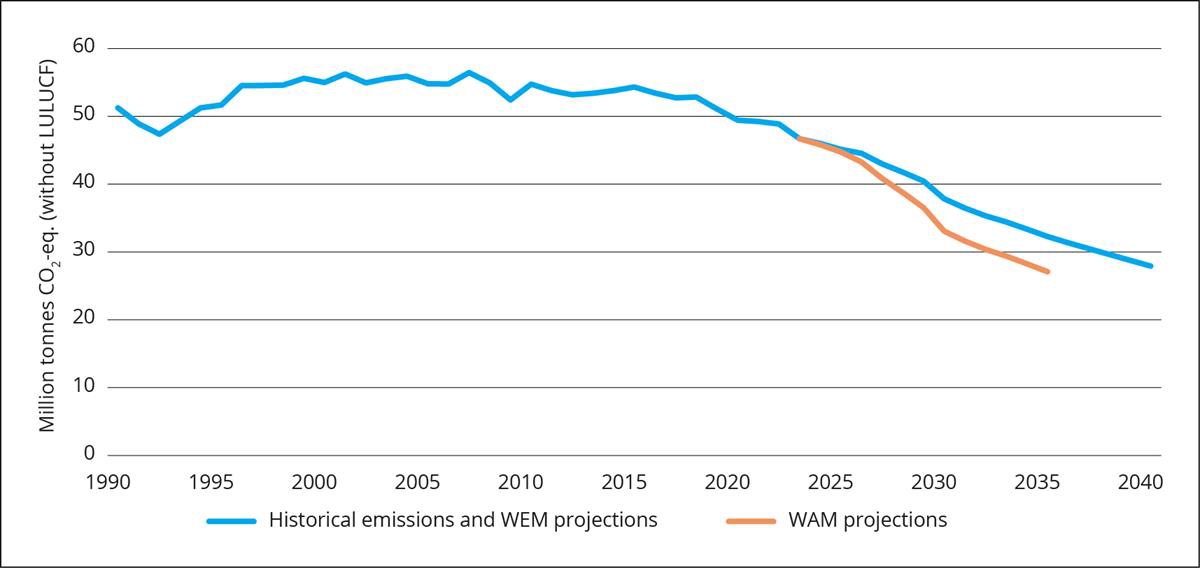

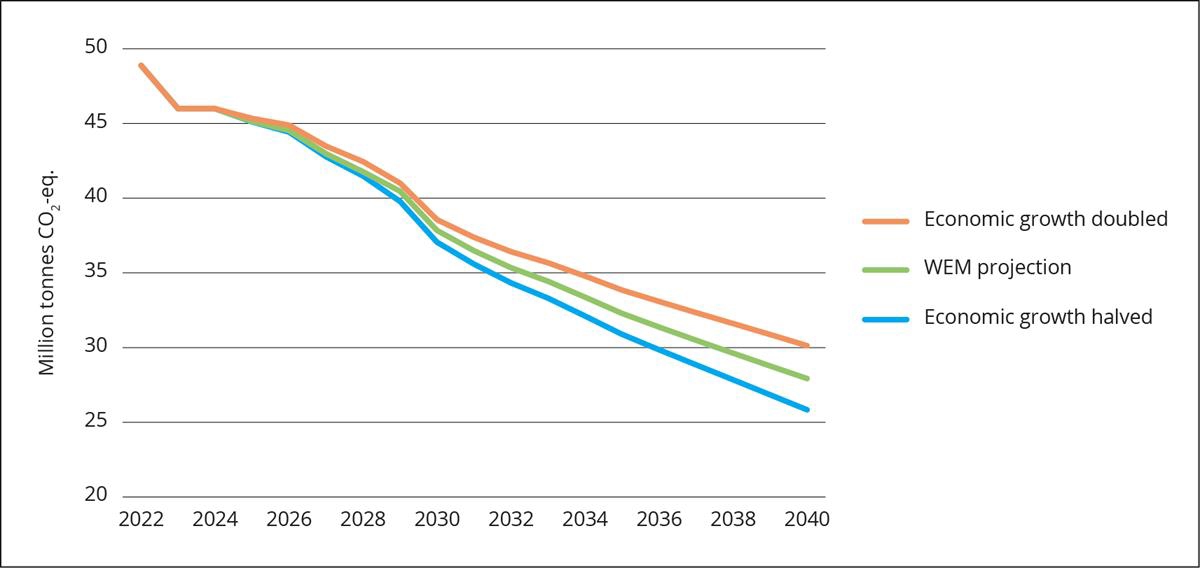

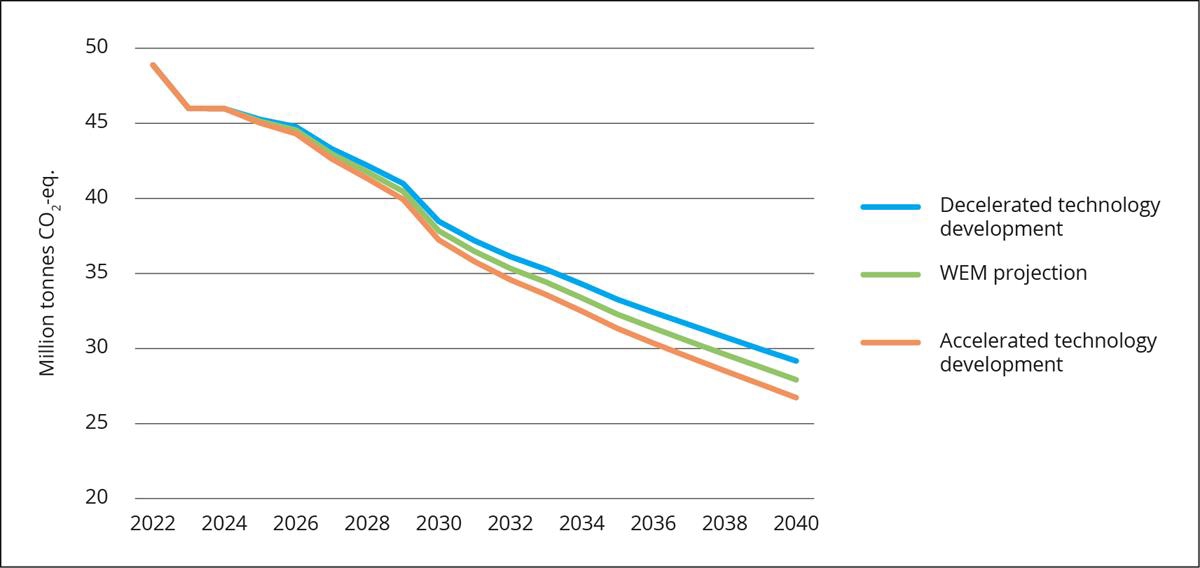

Norway has selected the indicator «emissions without LULUCF» as the indicator representing the point of departure in tracking progress towards the implementation and achievement of Norway’s NDC. This includes the emissions of indirect CO2. Norway’s with existing measures (WEM) projections (see chapter 2.7) shows that emissions without LULUCF could decrease to a level of 26.2 per cent lower than in 1990. Table 2.7 shows the projected values for Norway’s key indicator and these are identical to the values in the WEM projections without LULUCF.

Tabell 2.7 (CTF table 10) Projections of key indicator

Key indicator(s)c

Unit, as applicable

Most recent year in the Party`s national inventory report, or the most recent year for which data are available

Projections of key indicators

2022

2025

2030

2035

2040

Emissions without LULUCF

kt CO2 quivalent

48 879.49

45 137.64

37 842.04

32 283.55

27 915.49

Notes: The Party could add rows for each additional key indicator.

Further mitigation actions are planned and the with additional measures (WAM) projections (see chapter 2.7.6) show that domestic emissions without LULUCF could decrease 4.8 Mt further to a level of 35.5 per cent lower than in 1990. These 4.8 Mt refer to measures in the sectors covered by the ESR and would bring Norway closer to realizing the ESR budget. The government aims to close any remaining ESR gap with units acquired from EU countries. The government has set aside funding for such acquisitions and is exploring possible supply.

Assuming that the ESR target is met, emissions from the ETS sectors would represent the bulk of the remaining gap between actual emissions and the NDC target. Norway expects most, if not all of this gap to be covered by ITMOs representing a net flow of allowances between EU and Norway within the ETS. Additional removals and emissions from the LULUCF sector will also be accounted for towards the target. In the event that these contributions do not fully realize the target, Norway will account for ITMOs from countries outside the EEA. Funding for such acquisitions is available through the state budget; see Norwegian Global Emission Reduction Initiative – regjeringen.no. Note that an annual emissions balance consistent with chapter III.B (Application of corresponding adjustment) will be provided in a subsequent BTR, based on the annual information that will be reported under Article 6.2. For expected content in such forthcoming reports, see the previous subchapter.

2.5 Mitigation policies and measures, actions and plans

2.5.1 Introduction

The main instruments of Norwegian climate policy are cross-sectoral. This includes taxes on greenhouse gas emissions and emissions trading. Use of these instruments will contribute to fulfilment of emission targets at lowest cost to society. In addition to instruments that put a price on emissions, the Government uses other policy instruments to reduce barriers and correct market failures related to technology development, and in specific markets. An effective transition requires combinations of measures. Pricing emissions forms the basis as a continuous incentive to reduce emissions. Since most climate measures face multiple barriers, a single measure is rarely sufficient. Support for research and technology development is important to bring about necessary new solutions for emission cuts, and taxes and regulations can be crucial to ensure that such solutions are actually implemented. Notification of regulation, in combination with support during a transition period, can be particularly effective, as support can accelerate the impact of announced requirements and additionally increase acceptance of such requirements.

This chapter describes some of the most important policies and measures (PaMs) for reducing greenhouse gas emissions in Norway. The chapter consists of textual descriptions of cross-sectoral and sectoral PaMs. Information on PaMs is also presented in CTF table 5 in accordance with decisions 18/CMA.1 and 5/CMA.3. PaMs with a * in CTF table 5 are considered to be reflected in the WEM-projection while the PaMs described in chapter 2.5.11 are included in the WAM-projection. Annex 3 of this BTR describes the methodologies and assumptions used to estimate the GHG emission reductions or removals and where relevant information related to costs, non-GHG mitigation benefits and how the mitigation actions interact with each other.

2.5.2 Cross-sectoral

The Norwegian system of pricing GHG emissions

Important instruments of Norwegian climate policy are taxes on greenhouse gas emissions and emissions trading. Both these instruments put a price on emissions and make it more expensive to release greenhouse gases. Taxes provide an incentive to reduce emissions both through immediate action and through investment in research and development that will make it possible to reduce emissions at a later date. Cross-sectoral economic policy instruments (climate taxes) form the basis for decentralized, cost-efficient and informed actions, where the polluter pays.

CO2 taxes on mineral oil, petrol and emissions from petroleum extraction on the continental shelf were introduced in 1991 to cost-efficiently limit greenhouse gas emissions. In addition to being subject to CO2 taxes, emissions from extraction of petroleum were also included in the European emission trading system (EU ETS) in 2008. CO2 taxes on natural gas and LPG were introduced in 2010.

In Norway, taxes on GHG emissions and quotas (EU ETS) cover approximately 85 per cent of greenhouse gas emissions. The system of taxes on GHG emissions consists of the CO2-tax on mineral products (petrol, mineral oils, natural gas and LPG), the CO2-tax on petroleum activities on the continental shelf, the tax on HFC and PFC, the tax on waste incineration and the tax on SF6. The different taxes are harmonised, and in 2024, the standard tax rate on non-ETS emissions is 1 176 NOK per tonne. The tax rate on non-ETS emissions in the tax on waste incineration is 75 per cent of the standard rate for non-ETS emissions.

The price on greenhouse gas emissions varies between sectors and sources. The price on emissions is highest in the petroleum sector and in domestic aviation, which are also part of EU ETS. Both sectors are subject to taxes in addition to the EU ETS, and the total price on emissions is approximately NOK 1,500 per tonne of CO2 in 2024. Emissions of methane or nitrous oxide from agriculture is not a part of the EU ETS, nor is it subject to tax on. However, standard rates of CO2 tax and base tax on mineral oils apply to agriculture.

If natural gas and LPG is used in land-based manufacturing covered by EU ETS, the tax rate will either be reduced, or the activities may be exempted from the tax. For the time being, other sectors and activities exempted from the CO2 tax on natural gas and LPG include (list not conclusive) fishing in distant waters, chemical reduction or electrolyses, metallurgical and mineralogical processes and international shipping and aviation. In the 2025 budget, it is proposed to introduce a reduced and separate tax rates for emissions from fishing in distant waters and international shipping. The Norwegian parliament has adopted a tax on chemical reduction etc., but the tax will only be put into effect in the case where an exemption for emissions covered by the ETS is accepted by The EFTA Surveillance Authority (ESA).

Overall price levels have increased due to increases in the tax rates and the increase in the price of allowances in the EU ETS. In the period 2020 to 2023, the reduced rate for fisheries in domestic waters has been abolished, a new tax on emissions from waste incinerations is introduced, the CO2 tax on mineral products has been expanded to include emissions from the greenhouse industry and there is introduced a tax on SF6. It is further proposed base extensions for 2025.

Some taxes that do not target greenhouse gas emissions directly nevertheless increase the total tax on fossil fuels and therefore affect emissions. The road usage tax on fuels is levied to internalise the costs inflicted on the society in terms of accidents, congestion, noise, road wear and tear as well as health and environmentally harmful emissions other than CO2. In recent years, the road usage tax has been reduced to compensate drivers for the increased CO2 tax.

PaM cross-sectoral No. 1

The CO2-tax on mineral products (excluding road transport and air transport under the ETS)

The standard tax rate on emissions under the ESR is NOK 1 176 in 2024. The tax covers close to 100 per cent of all use of fossil fuels covered by the ESR.20

The CO2-tax on emissions from road transport and emissions from aviation covered by the ETS are treated as separate policies and reported under transport below.

PaM cross-sectoral No. 2

EU Emissions Trading System (ETS)

Norway established a national emissions trading scheme in 2005. Most features of the scheme closely resembled the EU’s emissions trading scheme (EU ETS) and covered 11 per cent of total Norwegian greenhouse gas emissions, mainly from industry. Emissions already subject to CO2 tax were not included in the scheme.